Asana + Monday: A Tale of Two IPOs

Why has Monday's stock outperformed Asana's since their IPO ~3 Years ago?

Asana and Monday.com are both work management tools.

They both serve a market of one billion knowledge workers.

Both received 100s of millions in funding pre-IPO.

Both went public within ~9 months of each other.

That’s where the similarities diverge.

Since Monday’s IPO, Monday’s share price has outperformed Asana’s by over 80%.

Monday is a darling of Wall Street while Asana is trading below the median of SaaS companies.

Why have these two companies’ performances and fortunes diverged and how can Asana reverse the trend?

Read more to learn about a tale of two work management tools ~3 years post-IPO

Part 1: Stock Performance

Since Monday.com went public, its stock has grown by 21% while Asana’s share price is down (62%).

An 80%+ outperformance!

Monday’s outperformance hasn't been consistent though. There have been three distinct phases of performance:

Phase 1: 🚀 ZIRP Era (ZIRP = Zero Interest Rate Policy)

Investors focus on growth at all costs.

Asana stock outperforms at the peak

Phase 2: 🪽Purgatory

Perform in-line as price search takes time

Phase 3: 🌤️ Monday’s Efficiency Rewarded

Investor focus on balancing growth with profitability.

Monday outperforms by 75%+ during this period

The relative valuation multiple of these two public companies has also differed depending on the phase. In the ZIRP Era, Asana actually traded at a premium to Monday.com. In the purgatory period of 2022, when the market was searching for the right price and valuation framework, Monday and Asana mostly traded in-line with each other. Currently, in the post-ZIRP era, Monday’s efficiency is rewarded and trades at a ~95% premium to Asana.

Lets dive into each phase in detail to understand why stock price performance valuation multiples for these companies has changed over time.

Part 2: Financials

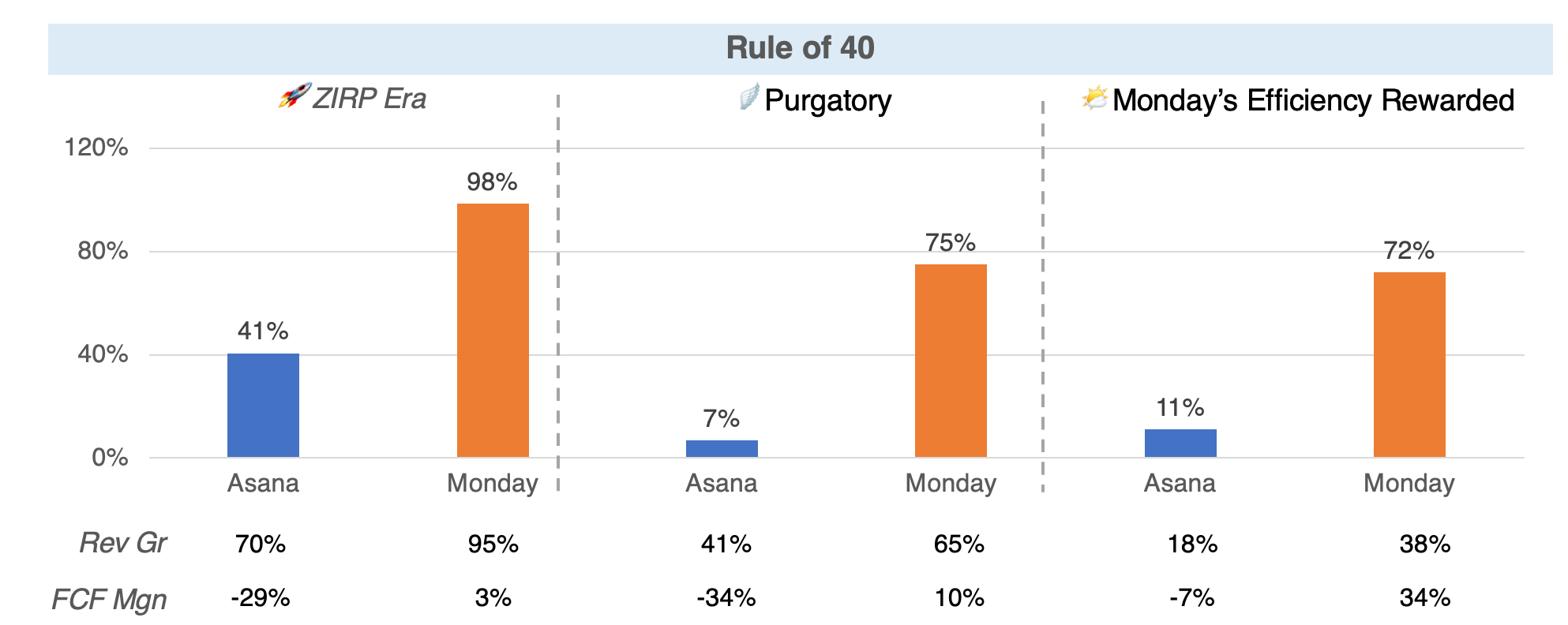

We can look at a number of metrics to evaluate financial performance. The most straightforward approach is to look at the Rule of 40 - which measures how companies balance revenue growth and profitability. As a reminder, the heuristic for the rule of 40 is that a company’s YoY revenue growth + free cash flow (FCF) margin should be at least 40. For example, if a company is growing at 40% YoY, the profitability can be 0% to achieve the rule of 40. Alternatively, a company with 80% YoY growth can have -40% FCF margins and still achieve the rule of 40.

The table above shows how each company balanced revenue with growth across the different phases. In the ZIRP Era, relative to Monday, Asana had a lower growth rate, a lower FCF margin and barely hit the rule of 40 benchmark, 41%. Monday on the other hand went against the grain during the period and was already FCF profitable, 3%, and had a rule of 40 of 98%. The market didn’t reward Monday for higher growth and profitability though - Asana was trading at almost 5 turns higher on revenue during this period(Asana valuation multiple of 52.3x vs. Monday valuation multiple of 47.4x).

I’m unclear on why Asana traded at a premium despite slower growth and lower profitability. If I had to speculate, I believe it’s because Asana’s CEO, Dustin Moskovitz, was a co-founder at Facebook, and has a reputation as a product visionary. Valuation during the ZIRP period was often driven by storyline and I believe the story of a Facebook co-Founder starting Asana led to Asana’s premium during this time period.

The market took time in 2022 to adjust valuation and stock performance expectations. During the 2022 Purgatory period Asana’s Rule of 40 went down to 7% with FCF margins worsening. Other other hand, Monday’s Rule of 40 went to 75% with FCF margins improving. Despite clear differences in operating metrics during this time period, Asana and Monday traded largely in-line with each other.

It took about a full year for the market to clearly favor Monday over Asana. In 2023, the market finally rewarded Monday with a premium valuation for balancing revenue growth with profitability and building a strong core business. Today Monday trades at a ~95% premium over Asana - trading at 11.2x NTM revenue while Asana trades at 5.7x revenue.

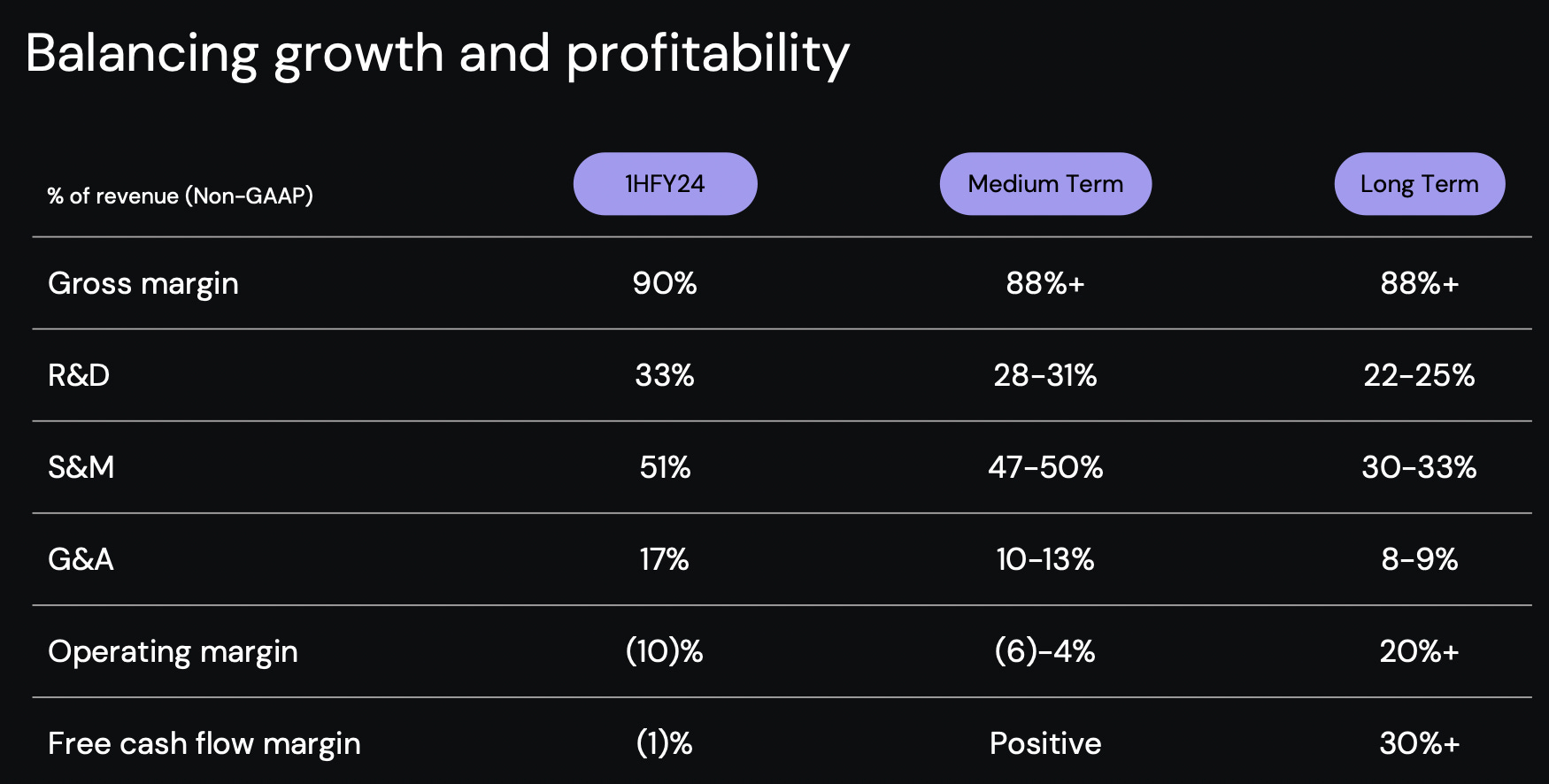

To complete the picture, I think it’s also instructive to take a look at Asana’s guidance from its October 2023 Investor Day to understand the premium that Monday has earned. In the guidance below from Asana, two things pop out to me. First, the company talks about balancing growth and profitability in the title but doesn’t share any growth numbers. Not sharing revenue growth implies to me that the company doesn’t have much confidence in it’s ability to reinvigorate growth in the future. Second, Asana’s has a long-term FCF target of 30%, which seems solid until you realize that Monday’s FCF margin is already at 34% (Q3’23)1.

My Takeaways

Monday is a proven story while Asana is a “show me” story. Monday is already showing healthy FCF margins, 34%, while growing at a healthy clip, 38%. On the other hand, Asana has ambitions of becoming FCF positive in the “medium term” and the company is trying to get to 20%+ revenue growth.

Credit: giphy.com Being outside of the Silicon Valley bubble can be an advantage. Monday is based in Israel where access to capital - relative to Silicon Valley - can be more challenging. This can lead to companies forcing themselves to be more prudent with their cash because raising capital is tough in these environments. Monday was profitable at IPO, at a time when being profitable wasn’t much of a driver of valuation multiples.

Price search can take time. Even though growth markets peaked in November 2021, it took most of 2022 for investors to recognize that Monday should trade at a premium to Asana. It took time for the market to align on how to reevaluate growth stocks in a post-ZIRP world - these periods of market shifts are when investors can find opportunities.

Part 3: Market Opportunity

Moving on from financials, let's dive into market opportunity. Both companies compete in the collaborative work management market, a $45B market according to Gartner. A large market but one that is dominated by Microsoft and Google, with a number of emerging competitors entering the space. Every few years there is a “hot” company in the space and eventually that company get supplanted by the next new thing. In the early 2010s the hot company was Dropbox, then we saw the emergence of players like Trello, Coda and Quip. Then came along Monday and Asana. Now, Notion is the hot emerging company in the market. Ultimately, the product set here is not very sticky and switching costs to new products are low.

So if Monday and Asana are both in the same market how does that impact relative valuation?

While Asana continues to play in only the work management market, Monday has grown its Total Addressable Market (TAM) by entering new adjacent market. Over the past ~18 months Monday has expanded into three new markets - CRM, Dev and Service Management. The company’s growth runway is supported by its ability to penetrate into these three large markets and now has a 2x market opportunity versus Asana.

Investors rightfully focus on a company’s ability to grow TAM since trying to win share within an existing market is expensive and risky. Companies that can grow into new markets are able to sell additional products into their existing customer base, resulting in higher ARPU and higher revenue. Additionally, these companies diversify revenue streams and de-risk their dependence on one market.

My Takeaways

Investor are rewarding Monday’s TAM expansion. Monday has increased its TAM >2x over the past 18 months and this gives the company additional revenue growth runway for the next decade. These new products are still nascent so right now they represent an option value to investors - Monday will need to execute and build real new businesses to get additional credit (i.e., valuation premium).

Monday is shipping products like they’re FedEx. Expanding into 3 new markets with three new products within ~18 months is very impressive and underpins the company’s ability to execute.

Part 4: Execution

Before we wrap up, let’s briefly talk about Monday’s execution. The company has out-executed its competition on two front. First in terms of delivering new products + features and second on efficient GTM growth.

Product

Monday has an impressive set of product innovations and features it has executed upon since founding.

So what drives the company’s exceptional product execution?

Unique product architecture. The company has built a robust platform with powerful low-code/no-code building blocks. These simple building blocks make it easier and faster to build new features onto the Monday.com platform. Additionally, the company has been able to launch the Dev and Sales CRM products, sharing 80% of the same code as the core Work product. In fact, the first version of Monday Sales CRM was built with four developers.

Flexible underlying technology. In traditional software architecture, developers start with defining the database, then build a UI to reflect it. Monday’s database schema on the other hand is built dynamically by users allowing flexibility in the application.

Culture. The management team has clearly developed a culture of shipping new products with high velocity. The company is known for fast, iterative execution and it shows in the company’s product innovation. Being one of the most desirable employers in Israel, a hotbed of technology talent, allows the company to pick some of the best talent from the region.

GTM

In addition to product innovation and efficiency, the company is known as one of the most efficient companies from a GTM standpoint.

Early in the company’s history, Monday developed a system called “Big Brain”, an internal BI tool that became the basis of the company’s data driven culture. Big Brain helps marketers make efficient performance marketing decisions. In the company’s early years, the company built a company with strong unit economics because of the early investments in Big Brain and efficient performance marketing. This efficient performance marketing engine was coupled with a self-serve go-to-market motion which enable the company to win in the SMB segment.

Over time, the company has slowly added sales teams and partners to support their self-serve motion, especially for larger customers. The company has also relied on a land and expand strategy to help grow existing customers on the platform. The table below shows how Monday has evolved its GTM motion over time.

Part 5: Wrapping Up + Asana’s Bull Case

To recap, why does Monday trade at a premium to Asana?

Management team known for balancing revenue growth with profitability

Proven ability to expand it’s TAM

Efficient GTM motion

Consistent product innovation

So what’s the bull case for Asana? If Asana seeks to turn the tide, a few things need to happen:

Executing against its AI vision. Asana has made strong improvements in its AI capabilities and the company is clearly putting a lot of effort here. Improving the product by using AI technology can help the company build a superior product to Monday and potentially displace it.

Nail the up-market strategy. The company already generates more revenue from $100K+ ACV customers than Monday because of an increased focus on enterprise customers. Asana can look to own this attractive segment of the market, resulting in better margins and improved growth.

Operational discipline. The company is still unprofitable and the company would benefit from borrowing from the operational and cost discipline that defines Monday.

To be fair, Monday is guiding to mid-20s FCF margins in their base case for 2024-2026 vs. the 34% earned in Q3’23. Nonetheless, the point stands - Monday is largely delivering on balancing profitability and growth while Asana has much to prove here.